Constant transaction values

When working with and querying transaction data, the following numerical values are returned which represent the corresponding constant value.

This page has the following reference tables for constant values:

cardTypechargebackCycleclasscurrencyIdpaymentTypeprocessMethodrecoveryStatustransactionStatustransactionType

Card type (cardType)

The Nexio cardType parameter is used with the View transactions endpoint in the request and returned as a number in the response. You can only send values for 10, 20, 30, 40, and 50. And in the response, you will only get those values or null, depending on the card used in the transaction.

| Value | Card type name | Name in webhook |

|---|---|---|

| 10 | Visa | visa |

| 20 | MasterCard | mastercard or masterCard |

| 30 | Discover | discover |

| 40 | American Express | amex or americanExpress |

| 50 | JCB | jcb |

| null | Diners Club | null |

| null | Carte Blanche | null |

| null | Unknown | null |

Chargeback cycle (chargebackCycle)

The Nexio chargebackCycle parameter is used with the View a chargeback and View chargebacks endpoints.

This value includes what part of the cycle the chargeback is currently in.

| Value | Name | Description |

|---|---|---|

| 0 | Canceled | The dispute was canceled. |

| 1 | Initial | The cardholder, through their credit card issuing bank, has identified this transaction as being either suspicious, or the merchant didn’t deliver what they promised. The issuing bank has transferred the funds back to the cardholder. See the reason code to better understand the cardholder’s reasoning. At this point, the merchant has the opportunity to submit compelling evidence to dispute the cardholder’s claim. The production Nexio Dashboard makes submission of the dispute very easy and convenient. This submission is routed through the merchant’s processor and the merchant’s acquiring bank.

|

| 2 | Won | Based on the submission of the compelling evidence to dispute the cardholder’s claims in the chargeback (see Cycle Type 1: Initial), a reversal of funds is conditionally awarded to the merchant. If the chargeback does not progress further after 2 months, this typically means that the conditional reversal is made final. |

| 3 | Represent | The cardholder’s issuing bank has determined that the compelling evidence submitted in the merchant’s original dispute did not justify overturning the original chargeback (see Cycle Type 1: Initial). The conditional reversal of funds to the merchant (see Cycle Type 2: Won) has been overturned - meaning funds are debited from the merchant. The merchant has the opportunity to submit new compelling evidence to continue to dispute the cardholder’s claim. This submission is routed through the merchant’s processor and the merchant’s acquiring bank. At this time, this submission must take place outside of the Nexio Dashboard.

|

| 3.1 | Represent (Open) | The cardholder’s issuing bank has determined that the compelling evidence submitted in the merchant’s original dispute did not justify overturning the original chargeback (see Cycle Type 1: Initial). Funds do not move in this Cycle Type. The merchant has the opportunity to submit new compelling evidence to continue to dispute the cardholder’s claim. This submission is routed through the merchant’s processor and the merchant’s acquiring bank. At this time, this submission must take place outside of the Nexio Dashboard.

|

| 3.2 | Represent (Closed) | If the merchant did not attempt to dispute during Cycle Type 3.1: Represent (Open), then the chargeback advances to this Cycle Type automatically. If the merchant did attempt to dispute during Cycle Type 3.1: Represent (Open) and the issuing bank did not agree with the merchant's dispute, then the chargeback advances to this Cycle Type. The conditional reversal of funds to the merchant (see Cycle Type 2: Won) has been overturned - meaning funds are debited from the merchant. This decision is final. |

| 4 | Final | Based on the submission of the new compelling evidence to dispute the cardholder’s claims in the chargeback (see Cycle Type 3: Represent), a reversal of funds is awarded to the merchant. This decision is final. |

| 4.1 | Final (Closed) | Based on the submission of the new compelling evidence to dispute the cardholder’s claims in the chargeback (see Cycle Type 3.1: Represent (Open)), the issuing bank did justify overturning the original chargeback. Because funds were already conditionally rewarded to the merchant (see Cycle Type 2: Won), there is no movement of funds. This decision is final. |

NoteTo check the status of a chargeback, you should get in direct contact with the chargeback department. You can also get information in the Nexio dashboard, but it may not be as up-to-date.

Class (class)

The Nexio class parameter is used with the View transactions endpoint. It is part of the cardMetaData object and refers to the category of card used in the transaction.

| Name | Value |

|---|---|

| Credit | 1 |

| Debit | 2 |

| Charge card | 3 |

| Unknown | 4 |

Currency ID (currencyId)

The Nexio currencyId parameter is used with the View transactions endpoint.

| Name | Value |

|---|---|

| Australian Dollar | 036 |

| Canadian Dollar | 124 |

| Yuan | 156 |

| Yen | 392 |

| Won | 410 |

| Mexican Peso | 484 |

| Pound Sterling | 826 |

| US Dollar | 840 |

| Euro | 978 |

Payment type (paymentType)

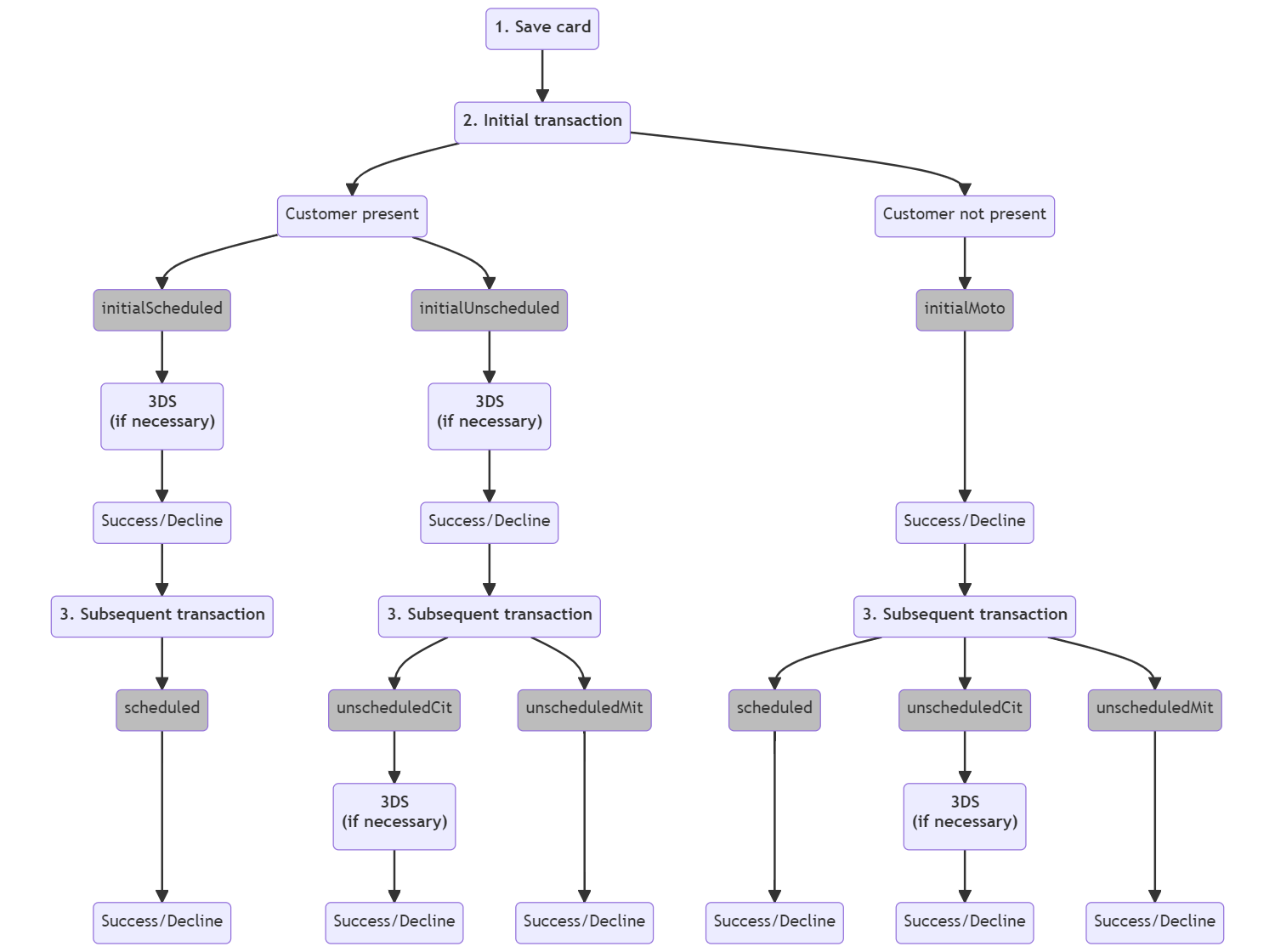

A payment type indicates the type of transaction being processed using stored payment credentials. This field is required to properly flag initial and subsequent transactions. Also, sending an incorrect value may result in fines to the merchant account from card schemes (Mastercard, Visa, and so forth). Please note that cardholder authentication (3D Secure) may be required depending on card issuer requirements.

Nexio defaults to initialUnscheduled for any of the following:

- When the security code is presented with the Run card transaction with iframe endpoint

- Retail keyed transactions (see Running a keyed transaction with the iframe)

- Retail terminal transactions (see Processing a transaction with a terminal)

- Virtual terminal transactions made in the Nexio Dashboard.

Nexio defaults to initialScheduled for any of the following:

- Initial transactions made through the Subscriptions service (see the Create a subscription endpoint)

- When the security code is presented with the Run card transaction endpoint

- When sending full card number (

card.pan) with the Run card transaction endpoint

Nexio defaults to scheduled for the following:

- When no security code is presented with the Run card transaction endpoint

- When sending full card number (

card.pan) andrecurringIdwith the Run card transaction endpoint

ImportantBecause Nexio sends a default, if you do not pass the

paymentTypeparameter and rely on the default value, any mislabeledpaymentTypethat results in declines, non-compliance, and/or fines will be the responsibility of the merchant.

You indicate a payment type when you run a card transaction by including processingOptions.paymentType in the body of your request. See the table below for possible values and explanations.

| Payment Type | Description |

|---|---|

| initialScheduled | Indicates a customer-initiated first transaction in a series of scheduled or recurring transactions. For subsequent transactions, use scheduled. |

| initialUnscheduled | Indicates a customer-initiated first transaction that is not part of a series of scheduled or recurring transactions. For subsequent transactions, use either unscheduledCit or unscheduledMit. |

| scheduled | Indicates a merchant-initiated subsequent transaction in a series of scheduled or recurring transactions. |

| unscheduledCit | Indicates a customer-initiated subsequent transaction that is not part of a series of scheduled or recurring transactions. |

| unscheduledMit | Indicates a merchant-initiated subsequent transaction that is not part of a series of scheduled or recurring transactions. Customer consent was provided at the time of the initial payment. |

| initialMoto | Indicates a transaction that is captured in a virtual terminal when customer card information is received over the phone, through mail, or via fax. If the initial transaction was initialMoto, the gateway or processor may not allow subsequent (such as recurring or scheduled) transactions for that payment method. For subsequent transactions that are supported by the gateway or processor, use scheduled, unscheduledCit, or unscheduledMit. |

Subsequent transactions

When we say "subsequent" transactions, we mean transactions that are meant to occur after a first transaction as part of a subscription or recurring situation where the customer is not present for that next transaction and you use a saved card token for that subsequent transaction.

This is not the same as a case where a customer would make a purchase once and then again in the future, whether with or without a saved card token. For those, each payment is either an initial transaction (initialUnscheduled or initialMoto) if getting the information from the customer directly each time, or an unscheduled transaction when using a saved card token after that first one (unscheduledCit if the customer selects their saved card or unscheduledMit if the merchant is running the transaction).

Otherwise, on subsequent transactions with a saved card token, use a paymentType of one of the following, depending on the situation:

unscheduledMit- The cardholder calls in to make a payment with a "card on file", regardless of thepaymentTypeused for the initial transaction.unscheduledMit- For situations like a cancellation or no-show fee that the merchant initiates.scheduled- When a cardholder enrolled in a series of payments.

Payment type flow

Example request

curl -X POST https://api.nexiopaysandbox.com/pay/v3/process \

-H 'Content-Type: application/json' \

-H 'Accept: application/json' \

-H 'Authorization: Basic [Base64_encoded_login]'

-d '{

"data": {

"amount": 1.15,

"currency": "USD"

},

"tokenex": {

"token": "6ee140a0-05d1-4958-8325-b38a690dbb9d"

},

"processingOptions": {

"paymentType": "initialScheduled"

}

}'Process method (processMethod)

The processMethod parameter gets returned with these endpoints:

The following table shows the possible values and what process method the code corresponds to:

| Name | Value |

|---|---|

| Card | 10 |

| Card Present | 11 |

| Card Not Present | 12 |

| APM (Alternative Payment Method) | 20 |

| Echeck | 40 |

| Credit | 50 |

| Cash | 60 |

Recovery status (recoveryStatus)

The table below describes the recovery statuses for transactions.

| recoveryStatus | Status | Description |

|---|---|---|

| 10 | Disabled | No retry attempt made. Can be enabled if the merchant account is configured for Decline Recovery service. |

| 20 | In progress | Transaction request has been sent to the gateway for processing. This is a temporary status. |

| 30 | Scheduled | The retry attempt has been scheduled. |

| 40 | Unrecoverable | The declined transaction cannot be retried. |

| 50 | Recovered | The transaction has been successfully retried. |

Transaction status (transactionStatus)

The table below describes the transaction statuses for card transactions. For echeck (ach) transactions, see Constant ACH transaction values.

Note

- The

transactionStatusreturned by the Payment service, including the Alternative payment method service will be a string.- The

transactionStatusreturned by the Transaction service will be an integer.

Card transaction status

| Status | Description | Nexio Dashboard Status | Transaction Service

| Payment Service

|

|---|---|---|---|---|

| Auth Only Pending | The payment is asynchronous and may receive a webhook notice with a status of authOnly in the future | AUTHONLYPENDING | 3 | authOnlyPending |

| Authorized Pending | The payment is asynchronous. The payment is pending and may receive a webhook notice with status of settled in the future | AUTHORIZEDPENDING | 9 | authorizedPending |

| Authorized | The transaction has been successfully authorized and is pending settlement | AUTHORIZED | 10 |

For new sandbox accounts, you can expect |

| Auth Only | The payment is Auth Only and capturing is required to receive the funds. The transaction can also be voided | AUTHONLY | 11 | authOnly |

| Declined | The transaction was declined | DECLINED | 30 | declined |

| Risk Hold | The transaction is pending due to fraud risk identified by the processor. Typically, these transactions get resolved within one business day, however, you can also contact Nexio Customer Support to get assistance. | RISKHOLD | 31 | riskHold |

| Fraud Reject | The transaction was declined by Kount prior to being submitted to the gateway | FRAUDREJECT | 32 | fraudReject |

| Settled | The transaction is settled. It can be refunded but not voided | SETTLED | 20 | settled |

| Void Pending | The payment is asynchronous and may receive a webhook notice with a status of voided in the future | VOIDPENDING | 39 | voidPending |

| Voided | The payment has been voided | VOIDED | 40 | voided |

| Error | An error has occurred | ERROR | 50 | error |

Transaction type (transactionType)

| Name | Value |

|---|---|

| Sale | 10 |

| Refund | 20 |

Updated 11 months ago